Islamic Financial Institutions (IFIs) are often discussed through the lens of individual products, such as Islamic banking accounts, sukuk, or takaful; however, this narrow view obscures a more important reality. At their core, IFIs are institutions with distinct structures, governance arrangements, and operating models that shape the functioning of Islamic finance.

Therefore, understanding Islamic finance begins not with contracts alone, but with the institutions that design, offer, regulate, and manage them.

This article (blog post) provides a clear and structured introduction to Islamic Financial Institutions as an institutional ecosystem. It explains what qualifies an institution as “Islamic”, the main types of IFIs, and how they differ from conventional financial institutions in terms of purpose and operation. The focus is on concepts and institutional roles rather than technical jurisprudence or sector-specific applications of the law.

Equally importantly, this post sets clear boundaries. It does not discuss how IFIs are used in housing, infrastructure, sustainability, or development policies, nor does it evaluate their performance or social impact. These areas require separate, focused analyses and will be addressed independently. The objective here is more fundamental: to clarify who IFIs are, what they do, and how the Islamic finance system is organised at the institutional level.

By the end of this post, readers will have a solid foundational understanding of Islamic Financial Institutions—how they are structured, the different forms they take, and why viewing Islamic finance through an institutional lens is the necessary first step before engaging with more advanced or applied discussions.

An institution is considered “Islamic” when its operations, products, and internal controls are designed to comply with Shariah rules regarding financial transactions.

This does not mean that it is a religious organisation or that it serves only Muslims. This means that the institution follows a different financial logic than conventional finance, and it applies that logic consistently through contracts, asset linkage, and ethical limits.

Contract-based finance rather than interest-based lending

Conventional institutions usually centre their business around interest-bearing loans. In contrast, Islamic Financial Institutions structure financing through clear contracts that specify what is being exchanged, how value is created, and how payments are made.

A simple way to think about it is as follows:

A conventional bank often earns money by charging interest on the money it lends.

An Islamic financial institution earns money through contracts tied to sales, leases, partnerships, or services.

This is why Islamic finance is often described as contract-based: the contract is the engine of the transaction, not the interest rate.

Linking finance to real assets and economic activity

The second defining feature is asset linkage. IFIs are expected to connect financial transactions to something real in the economy, such as an asset, service, project, or business activity.

This is important because it changes how institutions design their financial products. For example:

Financing may be tied to purchasing an asset and selling it on the agreed terms.

This may be linked to leasing an asset for a defined period.

Alternatively, it may involve investing in a business activity where returns depend on performance.

The core idea is straightforward: finance should not be detached from the real economy.

Operating within clear ethical boundaries

Another distinguishing element is the presence of ethical considerations. IFIs apply screening rules to avoid financing activities that are considered harmful or prohibited under Shariah.

In practice, this usually means avoiding sectors such as

Alcohol and gambling-related businesses

Pornography

Certain weapons-related activities

Other activities excluded under Shariah screening policies

The key point is not the specific list but the principle behind it: financial returns should not come from activities that violate the ethical limits defined by the system.

High-level Shariah oversight and internal controls

Finally, an institution is considered “Islamic” not only because it claims compliance but also because it typically has internal Shariah oversight mechanisms. These often include a Shariah board or advisory function along with compliance procedures.

At a basic level, this oversight aims to ensure the following:

Products are reviewed before they are offered

Operations follow approved structures

Any non-compliant income is identified and handled appropriately

The technical details vary by country and institution, but the concept is simple: an internal governance layer is dedicated to Shariah compliance.

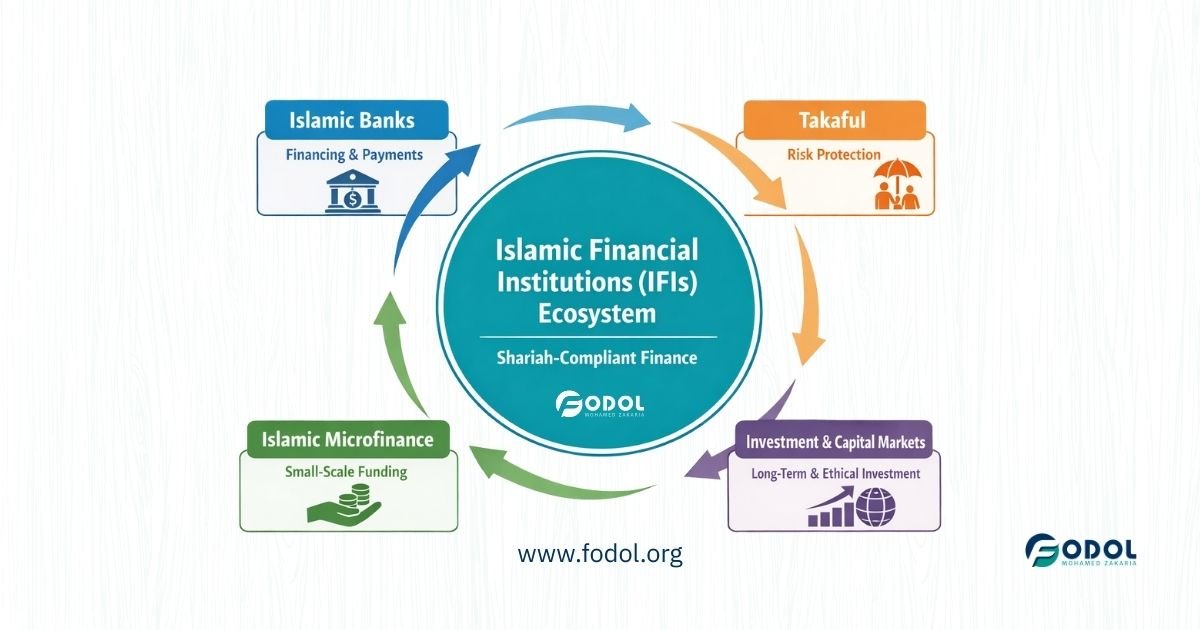

In practice, this institutional approach has several distinct forms. The Islamic finance ecosystem comprises different types of Islamic Financial Institutions, each serving a specific function.

The most common are Islamic banks, Islamic microfinance institutions, takaful operators (Islamic insurance), and Islamic investment and capital market institutions, such as asset management firms and sukuk-related entities. Understanding these institutional types is essential before examining their practical operations.

The Islamic Financial Institutions Ecosystem

Islamic Banks: The Core of the IFI System

Islamic banks are the most visible type of Islamic Financial Institution because they perform many familiar banking functions, safekeeping money, facilitating payments, and providing financing to households and businesses, while doing so through Shariah-compliant structures.

In simple terms, an Islamic bank is not “a bank that stopped charging interest.” It replaces interest-based lending with contract-based financing linked to real economic activity, supported by internal Shariah oversight.

What Islamic banks do (in plain language)

Islamic banks typically provide four core services.

Payment and transaction services: They offer current accounts, cards, transfers, payroll services, and business payment facilities, similar to conventional banks.

Safe-keeping and cash management: They hold customer funds and provide access to branches, ATMs, mobile apps, and online banking.

Financing for real needs: Instead of providing an “interest loan”, they structure financing through contracts tied to a purchase, lease, or partnership arrangement.

Investment intermediation: They pool funds from customers who want returns and deploy them into Shariah-compliant activities, then share profits according to pre-agreed rules.

Who Islamic banks serve

Islamic banks are not limited to a single category. In practice, they serve:

Individuals and families: salaries, payments, personal financing, home or car financing (structured through permissible contracts)

Small businesses and SMEs: working capital, equipment financing, trade-related financing

Large corporates: project and trade financing, treasury placements

Governments and public institutions: placements and sukuk-related services in some jurisdictions

The key point is that Islamic banks operate as full-service financial institutions; the difference lies in how they structure their products and manage risks.

How Islamic banks differ operationally from conventional banks

Deposits are not all the same: current vs investment: A common confusion is to assume that all deposits in Islamic banks behave like conventional deposits. In reality, Islamic banking typically distinguishes between current accounts and investment accounts, and they serve different purposes.

Current accounts (everyday money): These accounts are used for salaries, transfers, bills, and daily payments. In many Islamic banking models, the bank treats the funds as an interest-free loan from the customer, meaning the customer can withdraw at any time but does not earn a return.

Investment accounts (money placed to earn returns): These accounts are designed for customers seeking returns from Shariah-compliant activities. Returns are not guaranteed in advance and are generally linked to actual performance. Profits are shared according to agreed ratios, and losses—if they occur—are borne according to established rules.

A simple way to remember the distinction:

Current account: access and transactional convenience (no return expected)

Investment account: potential return linked to performance (not a fixed interest rate)

Financing instead of lending

This is the question most people ask: If there is no interest, what does an Islamic bank actually do?

The short answer is that Islamic banks finance through structured transactions, not interest-bearing loans.

In conventional banking, the logic is straightforward: money is lent and repaid with interest.

In Islamic banking, financing is structured around contracts tied to real economic activity, and profit comes from those contracts rather than from lending money itself.

In practical terms, this means:

The bank may buy an asset and sell it to the customer at a disclosed markup, paid over time.

The bank may purchase an asset and lease it for an agreed rental payment.

The bank may enter a partnership-style arrangement where returns depend on the performance of the financed activity.

The essential point is that profit is generated through defined contracts linked to real transactions, not through charging interest on money.

A quick comparison: Islamic banks vs conventional banks

To summarise the main operational differences clearly:

Basis of returns

Islamic banks: profit from contracts linked to assets or activities

Conventional banks: interest charged on loans

Treatment of deposits

Islamic banks: separation between non-return current accounts and performance-based investment accounts

Conventional banks: deposits typically earn predetermined interest

Relationship to real assets

Islamic banks: financing is generally connected to identifiable assets or services

Conventional banks: lending is often detached from specific assets

Ethical screening

Islamic banks: apply sectoral and activity-based ethical limits

Conventional banks: no uniform ethical restrictions

This comparison helps clarify a central point: Islamic banks remain banks in function, but differ in structure, incentives, and financial logic.

Islamic Microfinance Institutions

Islamic microfinance institutions represent a segment of the Islamic finance ecosystem that operates below the scale of commercial banking. While Islamic banks focus on individuals, firms, and governments with sufficient income or collateral, Islamic microfinance institutions are designed to serve low-income households, micro-entrepreneurs, and small informal businesses that are often excluded from formal banking systems.

Their role is not to replace Islamic banks, but to address financial needs that conventional and Islamic banks are usually not structured to meet.

What Islamic microfinance institutions are

Islamic microfinance institutions provide small-scale financial services using Shariah-compliant methods. These services typically include micro-financing, basic savings facilities, and sometimes micro-takaful arrangements. The key characteristic is scale: transactions are small, risks are managed differently, and relationships with clients are often more personal and community-based.

Unlike commercial Islamic banks, which operate as profit-driven financial intermediaries, Islamic microfinance institutions are usually mission-oriented organisations. They may be stand-alone entities, specialised units within larger institutions, cooperatives, non-profit organisations, or programs supported by charitable or social finance mechanisms. Their financial models are therefore simpler and more flexible, reflecting the realities of the communities they serve.

Who they serve

Islamic microfinance institutions typically target groups that face barriers to accessing formal finance, such as:

Low-income households needing small amounts of financing for basic economic activities

Micro-entrepreneurs operating informal or semi-formal businesses

Self-employed individuals with irregular income streams

Small traders and artisans who lack collateral or credit history

For these clients, the main challenge is not only affordability, but access and suitability. Islamic microfinance institutions are structured to work with clients who may not meet the requirements of commercial Islamic banks, while still operating within Shariah boundaries.

How they differ from Islamic banks

Although both are part of the Islamic finance ecosystem, Islamic microfinance institutions differ from Islamic banks in several important ways.

First, scale and complexity are much lower. Islamic microfinance institutions handle small transactions and simplified contracts, whereas Islamic banks manage larger, more complex financing arrangements.

Second, risk management is different. Islamic microfinance institutions rely more on close client relationships, group-based mechanisms, or community knowledge, rather than formal collateral and extensive documentation.

Third, institutional objectives Islamic banks are commercial institutions expected to generate profits for shareholders. Islamic microfinance institutions, while financially disciplined, are typically driven by social orientation—seeking to provide access to financial services rather than maximising returns.

Social orientation without policy claims

It is important to note that Islamic microfinance institutions are often described as socially oriented, but this does not mean they operate as charities. They still apply financial discipline, expect repayment, and manage sustainability carefully. The difference lies in emphasis: access, inclusion, and appropriateness of financial services take priority over scale and profitability.

At this stage, the key takeaway is institutional. Islamic microfinance institutions demonstrate that Islamic Financial Institutions are not limited to commercial banking models.

They form part of a broader ecosystem designed to accommodate different income levels, economic activities, and financial needs—using structures that remain consistent with Shariah principles while adapting to real-world constraints.

Takaful operators are Islamic Financial Institutions that deal with risk, a concept that exists in every economy but is often poorly understood in Islamic finance discussions. In simple terms, takaful is the Islamic alternative to conventional insurance. It is built on the idea that people protect one another collectively, rather than transferring risk to a company in exchange for a premium.

This difference in how risk is understood and managed is what makes takaful operators a distinct and often misunderstood type of IFI.

What takaful is, in simple terms

Takaful can be understood as a mutual protection arrangement. Participants contribute money into a shared pool, and this pool is used to compensate members who suffer a defined loss—such as damage to property, an accident, or a health-related expense.

Instead of buying insurance coverage from a company, participants in takaful are effectively cooperating to cover each other’s risks. The takaful operator manages this process on their behalf but does not own the risk pool in the same way a conventional insurer owns premiums.

A simple way to think about it:

In conventional insurance, risk is sold to the insurer.

In takaful, risk is shared among participants.

Understanding risk and why it matters in takaful

Risk, in financial terms, refers to the possibility of loss or uncertainty about future outcomes. Everyday examples include accidents, illness, property damage, or business disruptions.

In Islamic finance, risk is not something to eliminate entirely, because risk is part of real economic life—but it must be managed in a fair and transparent way. This perspective shapes how takaful works.

Common types of risk addressed by takaful include:

Personal risk (health issues, disability, death)

Property risk (damage, theft, fire)

Business risk (losses from unforeseen events)

Takaful operators manage these risks by:

Collecting contributions into a shared fund

Paying claims from that fund when covered losses occur

Managing the fund prudently and transparently

The key distinction is that risk is pooled, not transferred, and any surplus after claims and expenses may be shared with participants rather than kept entirely by the operator.

How risk-sharing differs from conventional insurance

In conventional insurance, the insurer takes on the risk in exchange for a premium. The company profits if claims are lower than expected and bears losses if claims exceed expectations.

In takaful, the operator:

Manages the risk pool on behalf of participants

Does not own the pool in the same way

Earns fees for managing operations, administration, and investments

This model changes incentives. The takaful operator’s role is closer to that of a manager or trustee than a risk-taking insurer. This structure is designed to align with Islamic ethical norms, which discourage uncertainty and unfair gain from others’ misfortune.

Why takaful operators are financial institutions

Although takaful is often described as “insurance,” takaful operators clearly qualify as financial institutions because they:

Collect and manage financial contributions

Invest funds in Shariah-compliant instruments

Manage financial risk and liquidity

Pay claims and administer long-term financial arrangements

In many jurisdictions, takaful operators are regulated alongside banks and other financial institutions, even if under separate insurance-specific frameworks. Their inclusion in the IFI ecosystem reflects their role in risk management, financial intermediation, and fund management.

A note on Islamic cooperative insurance

In some countries, most notably Saudi Arabia, takaful is often referred to as Islamic cooperative insurance. While this model draws inspiration from takaful principles, there are important differences in practice.

Literarily, takaful emphasises:

Mutual assistance

Collective risk-sharing

Participant ownership of the risk pool

Operationally, cooperative insurance models in some jurisdictions:

May resemble conventional insurance in structure

Often operate through shareholder-owned companies

Sometimes limit participant involvement in surplus-sharing

In short, not all Islamic cooperative insurance models fully reflect classical takaful structures, even if they are Shariah-compliant under local regulatory interpretations. The distinction matters because it affects how risk, surplus, and ownership are treated in practice.

Quick comparison: Takaful vs Conventional Insurance

Aspect

Takaful (Islamic Insurance)

Conventional Insurance

Core concept

Risk-sharing among participants

Risk transfer to insurer

Ownership of funds

Participants collectively

Insurance company

Role of operator

Manager/administrator of the fund

Risk-bearing insurer

Treatment of surplus

May be shared with participants

Retained by insurer

Ethical boundaries

Shariah-based screening

No uniform ethical restrictions

View of risk

Shared and managed collectively

Bought and sold

The key takeaway is that takaful operators show how Islamic Financial Institutions address risk differently, not by avoiding it, but by organising it around cooperation, shared responsibility, and ethical boundaries. This makes takaful a central, though often misunderstood, pillar of the Islamic finance ecosystem.

Islamic Investment and Capital Market Institutions: Completing the IFI Ecosystem

Islamic Investment and Capital Market Institutions form the long-term and market-facing side of the Islamic finance ecosystem. While Islamic banks focus on deposits and financing, and takaful operators deal with risk protection, these institutions are concerned with investment, asset allocation, and capital raising.

They channel funds from investors to governments and corporations through Shariah-compliant market instruments, making them essential for scaling Islamic finance beyond retail and commercial banking.

In simple terms, these institutions manage where money is invested, how capital is raised, and how investors participate in Shariah-compliant markets.

Islamic asset management firms

Islamic asset management firms are institutions that manage investment portfolios in accordance with Shariah rules. Their role is similar to conventional asset managers, but with an added layer of Shariah screening and oversight.

Institutional investors such as pension funds and endowments

Islamic banks placing surplus liquidity

Takaful operators investing participants’ funds

Their task is not only to generate returns, but to ensure that investments remain within ethical and contractual boundaries set by Shariah, which affects both asset selection and portfolio construction.

Islamic investment funds

Islamic investment funds are collective investment vehicles managed by Islamic asset managers. Investors pool their money, which is then invested in Shariah-compliant assets according to a defined strategy.

Common types include:

Equity funds (investing in Shariah-compliant companies)

The defining feature is that returns are linked to market performance, not guaranteed, and investors bear investment risk in exchange for potential gains.

Sukuk-related institutions

Sukuk-related institutions are those involved in the issuance, structuring, management, and distribution of sukuk, often referred to as Islamic bonds. While the technical structures of sukuk vary, the institutional role is clear: they enable governments and corporations to raise long-term funding from investors in a Shariah-compliant way.

These institutions include:

Issuing entities (governments, public agencies, corporations)

Special-purpose vehicles set up for issuance

Islamic banks and investment firms acting as arrangers or managers

Asset managers and funds that hold sukuk

Who uses sukuk:

Governments financing infrastructure, budgetary needs, or public projects

Corporations funding expansion or refinancing

Investors seeking predictable income streams within Shariah boundaries

Sukuk markets are therefore a key bridge between Islamic finance and global capital markets.

Understanding risk in Islamic investment and capital markets

Risk plays a central role in these institutions, but it takes a different form from both Islamic banking and takaful.

In this segment of the ecosystem, the dominant risks are investment and market risks, including:

Market risk: changes in asset prices or sukuk values

Credit risk: issuer ability to meet payment obligations

Liquidity risk: difficulty selling assets quickly without loss

Shariah compliance risk: assets becoming non-compliant over time

Unlike takaful, where risk is pooled and shared for protection purposes, investment and capital market risks are intentionally assumed by investors in pursuit of returns. Losses, if they occur, are part of the investment outcome, not events triggering compensation.

This also differs from Islamic banks, where risks are managed primarily through financing contracts and balance-sheet controls rather than market exposure.

How these institutions differ from takaful and other IFIs

The key distinction lies in purpose and risk orientation:

Takaful operators manage risk to provide protection against loss.

Islamic banks manage financing risk to support transactions and economic activity.

Islamic investment and capital market institutions manage investment risk to generate returns over time.

Each plays a different role, but together they form a complete financial ecosystem.

Quick comparison: Islamic capital market institutions vs other IFIs and conventional counterparts

Aspect

Islamic Investment & Capital Market Institutions

Takaful Operators

Islamic Banks

Conventional Capital Markets

Primary function

Investment and capital raising

Risk protection

Financing and intermediation

Investment and capital raising

Main instruments

Sukuk, Shariah-compliant funds, equities

Risk pools

Financing contracts

Bonds, equities, derivatives

Nature of risk

Market and investment risk

Pooled protection risk

Financing and credit risk

Market and speculative risk

Who bears risk

Investors

Participants collectively

Bank and clients (contract-based)

Investors

Return profile

Performance-based, not guaranteed

Not return-focused

Contract-based profit

Interest and market returns

Ethical screening

Mandatory (Shariah-based)

Mandatory

Mandatory

Not systematic

The key insight from this segment is that Islamic finance does not end at banking or insurance. Islamic investment and capital market institutions provide the mechanisms through which large-scale investment, long-term funding, and market participation occur, completing the institutional architecture of Islamic Financial Institutions.

How These Institutions Fit Together: Seeing Islamic Finance as a System

Islamic finance is often misunderstood because its institutions are discussed in isolation. Islamic banks are examined separately from takaful, microfinance, or capital markets, creating the impression that Islamic finance is a collection of unrelated entities. In reality, Islamic Financial Institutions are designed to function as an interconnected ecosystem, where each institution plays a distinct role while complementing the others.

Understanding this system-level interaction is essential. No single Islamic institution is meant to meet all financial needs on its own.

A layered financial system serving different needs

At the base of the system are Islamic microfinance institutions. They serve individuals and micro-entrepreneurs who operate at small scales and often lack access to formal banking. Their role is to provide simple, accessible financial services where commercial banking is not viable.

Above this layer sit Islamic banks, which act as the system’s core intermediaries. They provide transaction services, manage deposits, and structure financing for households, businesses, and public entities. Islamic banks connect everyday financial activity with larger pools of capital, making them central to the functioning of the entire ecosystem.

Alongside banking operate takaful operators, which address risk. Economic activity inevitably involves uncertainty, accidents, losses, and unexpected events.

Takaful institutions complement banking and investment by providing risk protection through collective pooling, helping individuals and businesses manage uncertainty without relying on conventional insurance models.

At the top of the system are Islamic investment and capital market institutions. These institutions manage savings over the long term and facilitate large-scale capital mobilisation. They channel funds into sukuk, investment funds, and Shariah-compliant market instruments, allowing governments and corporations to raise financing beyond the balance sheets of banks.

Each layer addresses a different financial function—access, intermediation, protection, and investment—while operating under a shared ethical and contractual framework.

How funds, risk, and roles move across the ecosystem

What makes Islamic finance an ecosystem rather than a set of standalone institutions is the flow of funds and risk between them.

Islamic banks may place surplus liquidity with Islamic investment funds or sukuk markets. Takaful operators invest participants’ contributions through Islamic asset managers. Microfinance institutions may rely on funding lines or support from Islamic banks or investment vehicles. In turn, capital market institutions depend on banks and takaful operators as major institutional investors.

Risk is also distributed across the system. Takaful absorbs certain types of uncertainty, banks manage financing-related risks, and investment institutions manage market risk on behalf of investors. No single institution carries all risks, and no single institution is designed to eliminate risk entirely.

Why Islamic finance is an ecosystem, not a single model

The defining feature of Islamic finance is not any one product or institution, but the way different institutions are structured to work together under shared principles. Each institution is specialised, limited in scope, and dependent on the others to function effectively.

This ecosystem approach explains why evaluating Islamic finance based on one institution—such as Islamic banks alone—often leads to incomplete conclusions. The system’s strengths and limitations only become visible when its institutions are viewed collectively.

In short, Islamic finance functions as a coordinated institutional architecture, where access, financing, risk management, and investment are distributed across different types of Islamic Financial Institutions. Recognising this interconnected structure is a necessary step toward understanding how Islamic finance operates in practice, beyond labels or isolated examples.

Common Misconceptions About IFIs

Misconceptions about Islamic Financial Institutions (IFIs) are not just “public misunderstandings. They shape expectations, regulation, and even product design. When IFIs are treated as either purely religious entities or simply conventional finance with new labels, the discussion becomes confused, and the analysis becomes unfair. The clarifications below address the most common myths in a direct and practical way, without technical debate.[1]

1) IFIs are only for Muslims

This is one of the most widespread misunderstandings. IFIs may have emerged to serve Shariah-sensitive demand, but they are not religious institutions, and they are not restricted to Muslim customers.

They are financial institutions operating under a defined compliance framework, much like ethical finance, socially responsible investment, or faith-based banking in other contexts. The core difference is the rules of transactions, not the identity of the client.[2]

A practical way to understand this is: if a product is structured as a permissible contract and the institution is regulated accordingly, anyone can use it—because the product is defined by its structure, not by the customer’s faith.

2) Islamic banks are charities, so they should offer cheaper finance

Many people assume Islamic banks exist mainly to deliver social welfare, so they expect them to behave like charities: low prices, flexible repayment, and “community-first” decisions even when the balance sheet cannot support it. This expectation is understandable, but it confuses Islamic banking with Islamic social finance.

Islamic banks are commercial institutions. Like conventional banks, they must manage liquidity, credit risk, capital adequacy, and operational costs. They are expected to be profitable and stable—especially because they hold deposits and provide payment services. That is why international institutions and regulators treat Islamic banks as banks, requiring comparable prudential oversight.[3]

This does not mean Islamic banks have no ethical dimension. It means their ethical commitments operate within commercial constraints. Social objectives—where they exist—often belong more naturally to institutions such as Islamic microfinance, zakat and waqf entities, or specialised social finance programs, not to commercial banks.

3) IFIs are basically the same everywhere

Islamic finance is often spoken about as if it were a single global template. In practice, IFIs differ significantly across countries because they operate within different legal systems, regulatory frameworks, and Shariah governance approaches. Standard-setting bodies such as AAOIFI and the IFSB provide guidance and standards, but adoption and implementation vary widely across jurisdictions.

This is why two institutions may both be “Islamic” while offering different products, using different governance arrangements, or applying different screening rules. The underlying idea is consistent, but the operational reality is shaped by national institutions and regulation.

4) There is no real difference between IFIs and conventional institutions

This claim usually comes in two forms:

Form A: It’s the same product with a different name.

Form B: Islamic finance ends up replicating conventional outcomes anyway.

There is a partial truth here, but it is often stated in a misleading way.

It is true that IFIs and conventional institutions often serve the same market needs, payments, financing, insurance, and investment, and therefore can look similar at the surface level. However, similarity in function is not the same as sameness in structure. IFIs are built around contract-based finance, asset linkage, ethical screens, and Shariah governance mechanisms that conventional institutions generally do not apply as a system-wide requirement.

At the same time, critics are also pointing to something real: in many markets, Islamic finance has relied heavily on instruments that behave economically like debt, which can make products feel familiar to conventional users. Even the World Bank has noted the need for IFIs to explore a wider range of Shariah contracts and innovate beyond debt-like financing patterns. [4]

So the accurate statement is this:

IFIs are not “identical” to conventional institutions, but in practice they may sometimes approximate conventional outcomes—especially where regulation, market expectations, and risk management push institutions toward simpler, more standardised structures.

5) Islamic finance is only banking

Another common misconception is to reduce Islamic finance to Islamic banks alone. In reality, the Islamic financial services industry includes banking, takaful (Islamic insurance), and Islamic capital markets, alongside investment funds and other supporting institutions. This broader ecosystem view is also reflected in how standard-setting bodies define the industry’s scope.[5]

This matters because focusing only on Islamic banks leads to distorted conclusions. Many of the system’s functions, risk protection, long-term investing, capital mobilisation—sit outside banking and are carried by other IFIs.

These clarifications are not defensive arguments. They are simply the baseline needed to understand IFIs accurately: what they are, what they are not, and why surface-level similarities can hide deeper institutional differences.

Key Takeaways for First-Time Readers

Before moving on to more detailed or applied discussions, it is useful to pause and summarise the core ideas covered so far. The following points capture the essential foundations needed to understand Islamic Financial Institutions clearly and accurately.

Islamic Financial Institutions (IFIs) are regulated financial institutions that operate according to Shariah-compliant rules. They rely on contract-based transactions, link finance to real economic activity, apply ethical boundaries, and are supported by internal Shariah oversight. They are institutions in their own right, not simply alternative financial products.

The Islamic finance system is made up of several institution types, each with a defined role: Islamic banks provide financing and payment services; Islamic microfinance institutions focus on small-scale and access-oriented finance; takaful operators manage risk through collective pooling; and Islamic investment and capital market institutions handle investment management and capital raising.

The difference between IFIs and conventional institutions lies in structure, not in function. Both systems offer similar financial services, but IFIs use contractual mechanisms instead of interest-based lending, apply ethical screening, and operate under a dedicated Shariah governance framework.

Understanding these distinctions matters because Islamic finance cannot be assessed accurately by looking at one institution or product in isolation. Seeing how IFIs are structured and how they fit together provides a clearer foundation for evaluating their strengths, limits, and real-world relevance.

Why Institutions Come First

Discussions about Islamic finance often move too quickly to judging results, impact, performance, or success, without first understanding how Islamic Financial Institutions are designed and how they operate. This shortcut creates confusion and misplaced expectations.

Before asking what IFIs deliver, it is essential to understand what they are, how they differ from conventional institutions, and how their structures shape behaviour and outcomes.

Institutions determine incentives, constraints, and possibilities. When their design is misunderstood, assessments of impact become superficial or unfair.

Seeing IFIs clearly at the institutional level is therefore the necessary first step, one that enables more meaningful analysis of performance, limitations, and future directions in the discussions that follow.

Mohamed Zakaria Fodol, Ph.D. is a researcher and writer specialising in Islamic finance, sustainable investment, and African economic development. His work explores how ethical finance can drive climate resilience and inclusive growth across emerging markets.

Dr. Fodol is the founder of FODOL.ORG, a policy-finance platform connecting ideas, research, and action for a sustainable global future.

I’m a researcher and writer exploring the intersection of policy, finance, and sustainability. My work focuses on Islamic finance, green investment, and Africa’s economic transformation. Through FODOL.ORG, I aim to make complex financial ideas clear, practical, and relevant for decision-makers shaping a sustainable global future.

{kind=link}